the most commonly used inventory costing method in the u.s. is:, check these out | Which inventory method is used by most companies?

By Sarah Rowe

By far the most popular inventory valuation methods are First-In First-Out, Last-In First-Out, and Weighted Average Cost. The generally accepted accounting principles (GAAP) in the States allow all three to be used.

Which inventory method is used by most companies?

First-In, First-Out (FIFO)

The FIFO method is the standard inventory method for most companies. FIFO gives a lower-cost inventory because of inflation; lower-cost items are usually older.

Which of these inventory methods are acceptable under US GAAP?

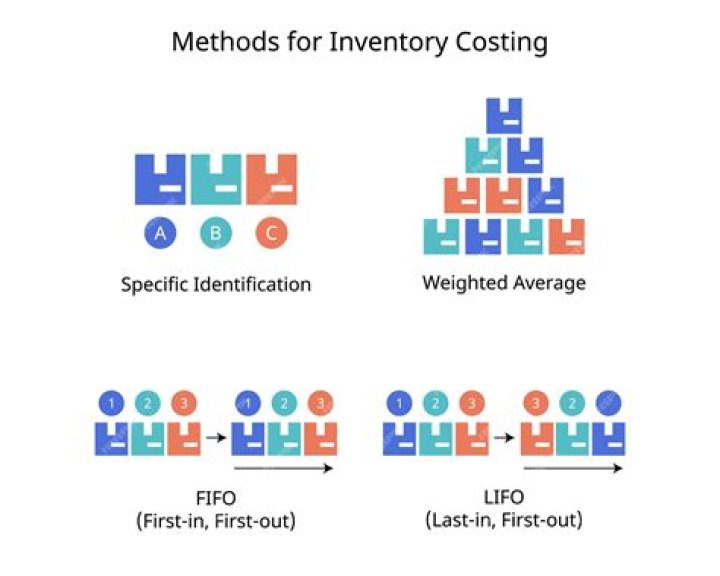

Under GAAP, FIFO (first in first out), LIFO (last in first out), weighted average, and specific identification are all acceptable methods of cost determination for your company’s inventory.

What is the best inventory costing method?

FIFO in restaurants

Of all inventory valuation methods, first-in, first-out is the most reliable indicator of inventory value for restaurants. Because this method corresponds inventory with its original cost, the calculated value of remaining goods is most accurate.

What is the most commonly used inventory method?

First-In, First-Out (FIFO)

The FIFO valuation method is the most commonly used inventory valuation method as most of the companies sell their products in the same order in which they purchase it.

What are the four inventory costing methods?

The four main inventory valuation methods are FIFO or First-In, First-Out; LIFO or Last-In, First-Out; Specific Identification; and Weighted Average Cost. We’ll dive deeper into these – but first, let’s go over some basics.

What is the retail method of inventory costing?

The retail inventory method is an accounting method used to estimate the value of a store’s merchandise. The retail method provides the ending inventory balance for a store by measuring the cost of inventory relative to the price of the goods.

How is inventory valued under US GAAP?

Under US GAAP, inventories are measured at the lower of cost, market value, or net realisable value depending upon the inventory method used. Market value is defined as current replacement cost subject to an upper limit of net realizable value and a lower limit of net realizable value less a normal profit margin.

What inventory costing methods are allowed by GAAP?

The GAAP accepts the three most common inventory valuation methods – FIFO, LIFO, and WAC – while the IFRS doesn’t accept the LIFO method.

Which costing method is allowed under GAAP?

One of the most basic differences is that GAAP permits the use of all three of the most common methods for inventory accountability—weighted-average cost method; first in, first out (FIFO); and last in, first out (LIFO)—while the IFRS forbids the use of the LIFO method.

What are the three main inventory costing methods?

The method a company uses to determine it cost of inventory (inventory valuation) directly impacts the financial statements. The three main methods for inventory costing are First-in, First-Out (FIFO), Last-in, Last-Out (LIFO) and Average cost.

What is standard inventory costing?

Standard Cost Inventory

Standard costing is when companies assign the expected (or standard) costs of material, labor and overhead to inventory, rather than the actual costs. This management tool helps to plan budgets, manage and control costs and determine how successfully a company controls cost.

Which inventory valuation method is most popular and why?

For most companies, FIFO is the most logical choice since they typically use their oldest inventory first in the production of their goods, which means the valuation of COGS reflects their production schedule.

Which inventory costing method produces the highest amount for ending inventory?

Conversely, FIFO gives you the timeliest value for ending inventory, since the unsold items reflect the most current costs. In periods of rising prices, FIFO leads to the highest income and taxes.

Which costing method gives the highest ending inventory the highest cost of goods sold?

Based on the table above, FIFO gives the highest cost for ending inventory. Since the cost of inventory increases the later date the company purchases goods, the inventory with higher costs forms part of the ending inventory.

What are the two main inventory methods used in process costing?

Both the FIFO and LIFO methods require the use of inventory layers, under which you have a separate cost for each cluster of inventory items that were purchased at a specific price.

What are the types of costing methods?

Different Methods of Costing – Single Costing, Job Costing, Contract Costing, Batch Costing, Process Costing, Operation Costing, Operating Costing and a Few Others

Single Costing, Unit Costing or Output Costing: Job Costing: Contract Costing or Terminal Costing: Batch Costing: Process Costing: Operation Costing:

What is inventory and its methods?

There are three methods for inventory valuation: FIFO (First In, First Out), LIFO (Last In, First Out), and WAC (Weighted Average Cost). In other words, whenever you make a sale, under FIFO, the items will be subtracted from the first list of products which entered your store or warehouse.

Related Archive

More in updates

harry potter wizards unite mod joystick, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023

harry potter vs voldemort poster, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023