can you buy a short sale with fha, check these out | Can you use FHA for a short sale?

By Jessica Wood

A seller can qualify for a Federal Housing Administration (FHA) short sale if the Department of Housing and Urban Development (HUD) determines the seller has a hardship. All FHA short sales are governed by HUD guidelines.

Can you use FHA for a short sale?

A short sale occurs as a compromise between a seller and her own lender. A seller who cannot make payments must face foreclosure or an alternative change in the loan. However, there is little preventing a buyer from using an FHA loan to purchase a short sale house.

Can I get financing for a short sale?

A short sale is a foreclosure prevention method. Unlike a foreclosure, the property is still owned by the seller. Financing a short sale is possible, provided you and the lender are willing to wait.

Why do sellers not want FHA loans?

The other major reason sellers don’t like FHA loans is that the guidelines require appraisers to look for certain defects that could pose habitability concerns or health, safety, or security risks. If any defects are found, the seller must repair them prior to the sale.

What is short sale approval?

A short sale is when a lender agrees to accept a mortgage payoff amount less than what is owed in order to facilitate a sale of the property by a financially distressed owner. The lender forgives the remaining balance of the loan.

Are short sales negotiable?

Are Short Sale Home Prices Negotiable? Short sale home prices are negotiable, but not in the same way as the sale price in a traditional purchase is. As the seller, you may be motivated to get rid of the property—but the mortgage lender must ultimately decide whether to accept an offer.

How can I remove a short sale from my credit report?

Write a letter to the credit bureau at the address on the credit report. Point out that the short sale listed on your report does not belong to you (the information is inaccurate) or is outdated and should be removed.

How long until a short sale falls off credit report?

Short sales, like foreclosures, can remain on your credit report for as long as seven years. The silver lining with short sales is that your score is likely to begin improving more quickly, usually in about two years.

How long does short sale stay on credit report?

How Long Does a Short Sale Affect Your Credit? A short sale could impact your credit scores as long as it remains in your credit reports, which may be up to seven years—similar to many other negative marks.

Do short sales hurt your credit?

Yes. There is no way to avoid the damage a short sale does to your credit score. A short sale can knock as much as 160 points off your credit score, but the level of damage heavily depends on your credit standing before the short sale and how much your lender gets in the sale, among other things.

Which of these lenders would be least likely to approve a short sale?

Which of these lenders would be least likely to approve a short sale? Junior lenders are least likely to approve a short sale. Because they’re in a secondary position when it comes to liens against the property, they realize that there may not be any money left to pay them after the lender in first position is paid.

What are the risks of a short sale?

7 Disadvantages of Buying a Short Sale

Long Process. Subject to the Mortgage Lender’s Approval. Lender Could Counter, Reject or Not Respond. Opportunity Cost. Property ‘As Is’ Is the Seller Approved? Lenders Prefer All Cash or Large Down Payments.

Do FHA loans take longer to close?

It takes around 47 days to close on an FHA mortgage loan. FHA refinances are faster and take around 32 days to close on average. FHA loans generally close in a very similar timeframe to conventional loans but may require additional time at specific points in the process.

Is it hard to get FHA approved?

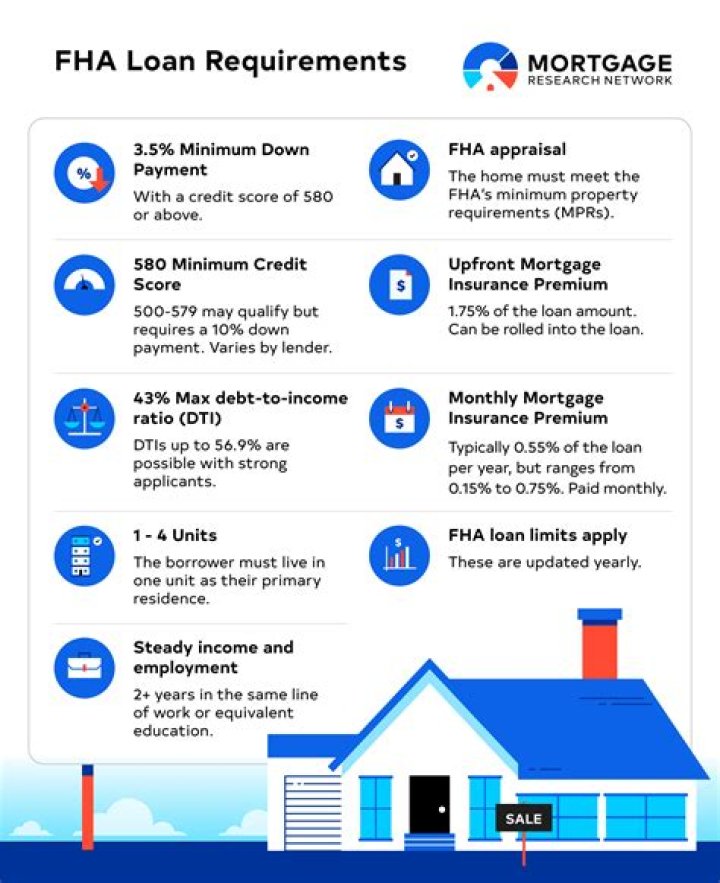

Read our editorial standards. To qualify for an FHA loan, you need a 3.5% down payment, 580 credit score, and 43% DTI ratio. An FHA loan is easier to get than a conventional mortgage. The FHA offers several types of home loans, including loans for home improvements.

How long do you have to keep a house with an FHA loan?

FHA loans are for owner-occupied property only. You must move into the property within 60 days of closing a purchase, and must occupy the property for at least one year.

Why would a short sale be denied?

A short sale is sometimes denied due to something as simple as the seller being current on paying their mortgage. The bank’s guidelines might state the bank isn’t allowed to approve a short sale if the mortgage payments aren’t in arrears.

How much do you offer for a short sale?

A price that’s 5% to 10% below market value is typically a good number to put on the table.

Do banks approve short sales?

Banks generally do not approve a short sale until the bank receives an offer from a buyer. Therefore, the usual way a short sale can be approved is for a buyer to submit an offer. The seller delivers the lender’s required documents to the agent. The buyer submits an offer subject to lender approval.

Related Archive

More in general

harry potter wizarding world japan, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023

harry potter vs voldemort in the deathly hallows, latest free online harry potter movies, best HD videos you should watch in 2022 – 2023